Technological Revenge Part 2

HEY! This ain’t in the brochure!

This next part will be difficult for many to swallow. It is the topic that prompts my comments elsewhere that I have been down the road we are now all currently traveling down, just in a different vehicle. I know where this road goes. The destination is not a place anyone wants to go to.

It is a topic that is a whole other universe of ideas, concepts, laws, regulations and consequences that are completely foreign to the American mind for certain, and possibly others. It is a topic that I have tried to warn others about as I seek aid in escaping from it. It is a topic that I have had the same success with “converting” anyone I know as I have in getting people to stop wearing masks against viruses, NONE. It is my opinion that lockdowns and such are but one step in a larger, longer process to enslave us all. While this focuses upon what the US has done and is doing, now that the US got the ball rolling, other counties are implementing their own versions. The OECD has its own Common Reporting Standards (CRS) that should terrify all who know of it. This post, as my last, is to give some idea of some of the steps that have been undertaken before covid was used to begin the current step.

This topic too has been with us for a long time, but ignored by many, including myself. From time to time there were whispers of it, but on the surface it seemed it did not apply to me nor anyone I knew. I ignored it. Renewing my US passport from Japan compelled me to dig deeper and I have spent much of the past 9 and 1/2 years studying this. As with Covid, what the experts say on the topic is at best incomplete and at worst, dangerous lies.

Instead of guiding you down the path from the beginning, let me first show where we are now.

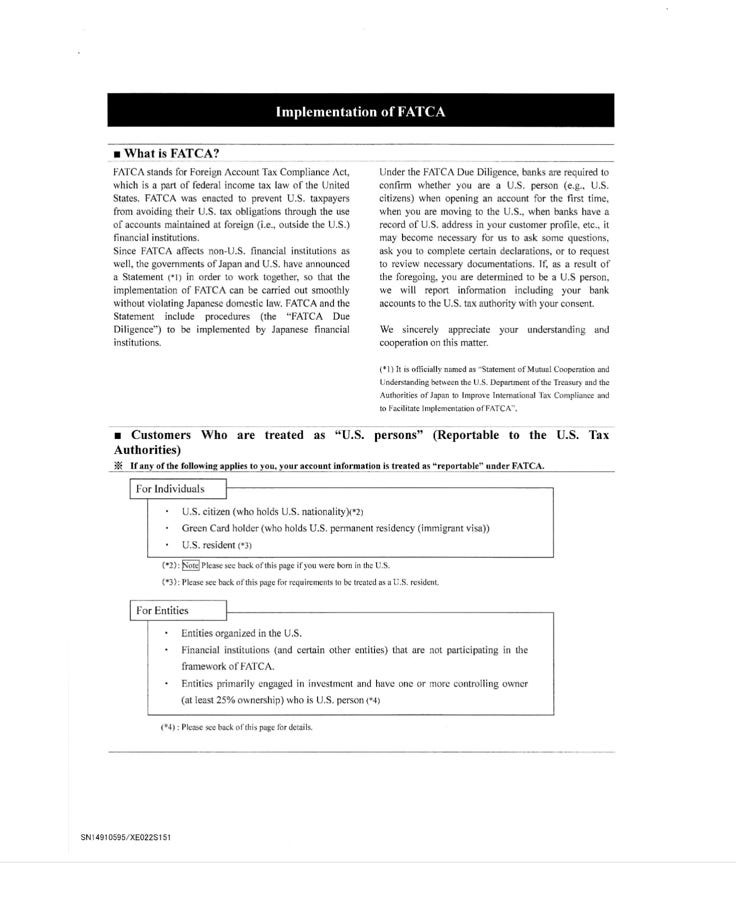

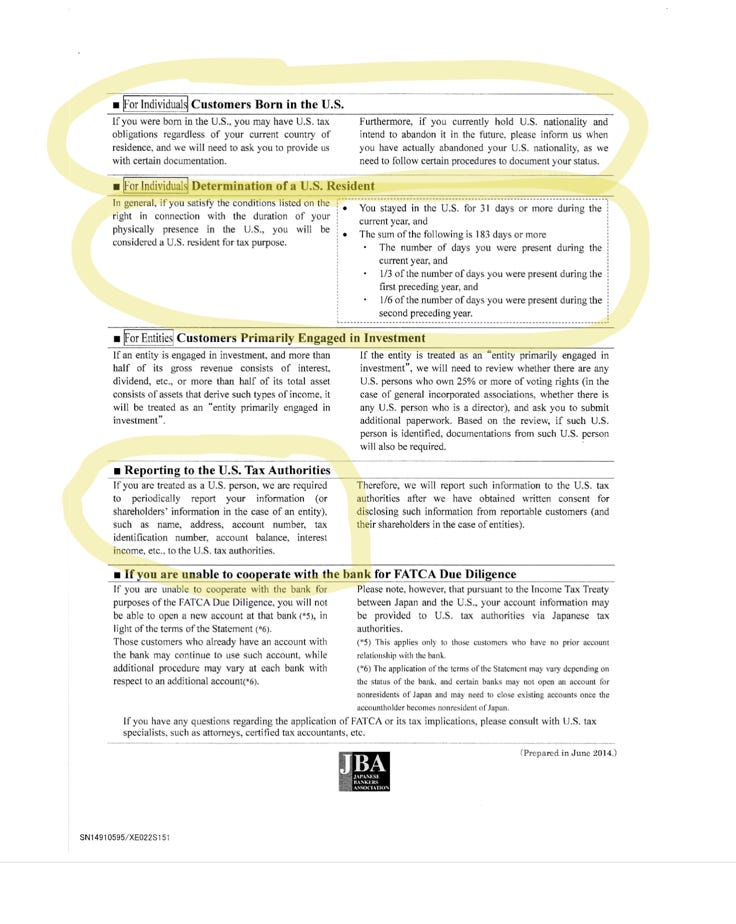

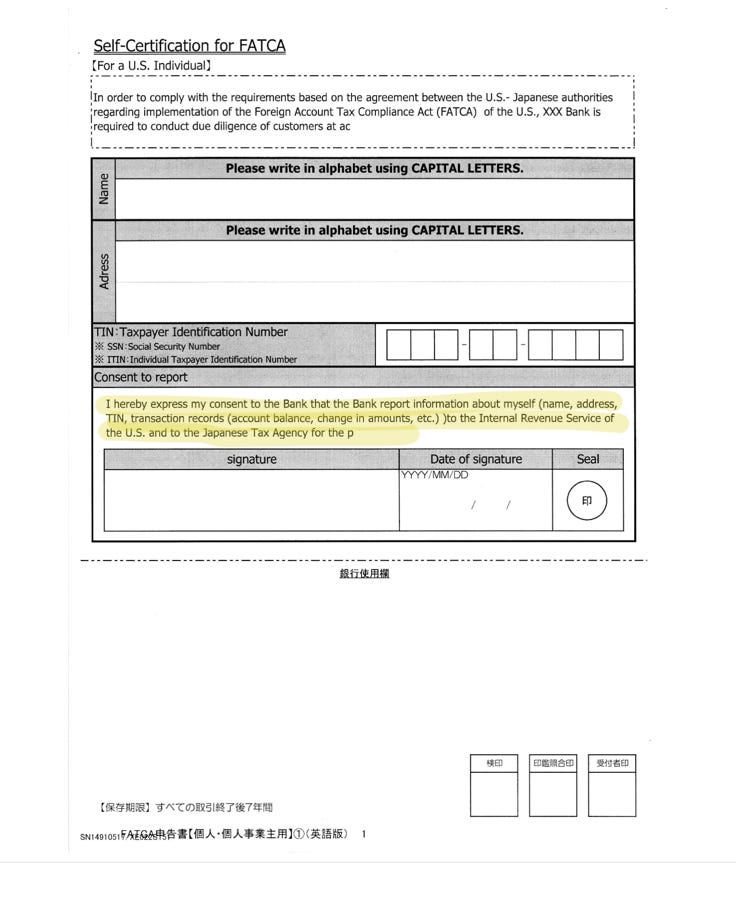

This is an example of what is called a “FATCA Letter”. It defies expert comments and opinions.

Please note who compiled this and when as shown at the bottom of the second page.

After much arguing about who is and not affected by FATCA, I opened a new account here in Japan just to find out. I was correct, the experts were wrong.

So what is all this about? Unbeknownst to most, US citizens (USCs) must file annual tax returns on income regardless of where they live or where the money was earned. The Foreign Earned Income Exclusion (FEIE) does NOT remove this obligation. Most of us, such as myself, who live outside the US and earn below the FEIE are required to file US federal income tax returns but do or did not know this. Take a look at the estimated number of USCs living abroad and compare that with the number of income tax returns from USCs living abroad an you’ll see that there is a huge gap between those who should and those who do. Under certain circumstances, we are also to spy on our family members’s, employers’ and civic groups’ finances and report these to US law enforcement via the FBAR. FATCA is the US law that the US compelled every nation on Earth to comply with to find out who is and is not filing the required tax and information returns. Yes, even China and Russia report the financial information they have on all US Persons with accounts in their countries. What’s this “US Persons” thing? There is not a single definition of who exactly is or is not a US person. One body of US law provides one definition while another gives a differing definition of the term. The one point they all agree upon is the all USCs are included in the broader term of US Person. Take a look again at the FATCA letter above to get a feel of who else may be a US Person. For USCs, this reporting is now linked to our passports. I very well be losing mine next year because of this.

Recently there has been a lot of discussion of the IRS requirement to report all transactions of $600. and more, rightfully so. However, no one seems to care that we (USCs) who live outside the US have each and every transaction reported to the US. Pay here in Japan is by direct deposit. Bills are paid via automatic withdrawal. All this is reported to the US. Not wanting any 3rd party involved in my everyday financial life, I had tried to pay as many of my bills in cash as possible. The entities I owe monthly bills to are not happy with this and charge me extra for paper bills. Recently it dawned on me that this has backfired. The bills come with a bar code. When I pay them at the convenience store, the clerk scans the bar code. Not only is the amount recorded, but also the store’s location and the time of the transaction as well as my name and address. Outsmarted myself, it would appear.

This too did not happen over night. I will use my own 30 year experience with cross boarder money transfers to shine a flashlight beam on the universes of dark matter that is government surveillance of all financial transactions.

While serving in the US navy in the late 80s through the early 90s, “Direct Deposit” was heavily promoted for all government employees. It still being optional at the time, I did not sign up for it. I knew then that to error is human but it takes a computer to really Fauci things up. I got to observe this when a shipmate received $1.42 each payday for several months. At first he was told, “We’ll fix this and you’ll get it along with regular pay next pay day.” Any error takes one full pay cycle to correct. But it was not fixed for many months. When I departed that command, he had had his and his wife’s credit cards cancelled as he had no many to feed his family and used them in the hopes of buying time until the navy got its shit together and paid him his back pay. I know that he had also received a repossession order for his car and was worried about being evicted. Like I said, t takes a computer to really fauci things up. Years later I would have the same problem working for the National Park Service after graduating college and before coming to Japan. By then, Direct Deposit was not an option. If I wanted to get paid, I had to accept it. I did accept it but was not paid. The first payday was 6 weeks late and incomplete. It destroyed me financially. Destroyed my credit rating too.

I first stared using International Postal Money Orders (IPMO) to receive money from my account in the States while studying in Japan in the mid 90s. The reason for using this method is cumbersome to describe. Basically, Japan’s banking system is not well integrated into the global banking system, at least it was not in the mid 90s. Cashing IPMOs was easy. I just took them to the post office and cashed them. If there were any interrogatory questions at the time, they were few and unintrusive. No more than ‘For what purpose is this amount being sent?’ or similar and whatever I wrote was excepted at face value. Later, once I started working here, I started using the same method to send money to the States. Reasons included gift money for anniversaries and Christmas, college loan payments and shortly after arrival this trip, credit card payments. Little by little, the questions became more and more intrusive and required ever more detailed responses. A shocking development come with a phone call from the central post office demanding details on an IPMO I sent years before. The reason I gave at the time of sending it was, “Credit card bill payment.” Years after the payment, they demanded that I tell them what I had purchased on my credit card that I paid for with the IPMO and how much I paid for each item; information I no longer had. Was this call due a then existing requirement that was overlooked or were they going through their records forcing past actions to conform with current rules? This hunts me still as just last week I exchanged US dollars my mother sent in cash in a Christmas card. On the form I had to declare how the cash I had came to be in my possession. It is illegal to send cash in envelopes. Yes, I know everyone does it for Christmas but that does not change the fact that it is illegal and I am being forced to choose between exchanging this Christmas money and admitting we broke the law or sending it back. I wrote, “From parents.” and hope I will not at some time in the future be called to explain further.

IPMO service no longer exists. Before it ended, the difficulty to cash them became increasingly greater. I had to declare on separate forms used by both Japan and the US, my relationship with the sender and detail why they sent the money. The last time I cashed one it was for $40., yes forty US dollars and was a birthday gift from my parents to one of my kids. The local post office could no longer cash IPMOs. It had to be sent to the central PO, who after calling me, approved it. I had to make a second trip at a later date to my local PO to receive it.

Due to my somewhat unique circumstances I have been forced to see some of what they are doing to us. I have my earning ability restricted through technology due to my citizenship. Business prospects have been declined because I will not allow myself to be a Trojan Horse for the US government against my potential clients. Anyone who would pay me would have at a minimum their names, addresses, email addresses, their relationship to me, the amount they sent and why they sent it reported to the US. If they send the money directly from their bank account, then their account number is also shared. This is not a possible future. This is not “will” or “may be”, it is “is”. This is the current situation and has been for a few years. However, this problem is no longer uniquely American. The OECD’s CRS seeks to do the same.

Next up; FinTch, Internet of Things (IoT) and international parcel post. Afterwards, I will attempt to illustrate where this all leads and how the covid panic fits in.

Oh, yeah. Here are some of the traitors to Japan's national sovereignty -- the WEF's puppets in the Center for the Fourth Industrial Revolution Japan:

https://initiatives.weforum.org/c4ir/japan

Ah, yes, the coming mandatory "digital ID". It is always portrayed by the "players" as a benefit to the person using it. But it is the path to total control and digital/financial slavery of humans by an oligarchy of the usual ruling elite. Economist Catherine Austin Fitts explains the Central Bank's "going direct" financial reset in this short video from 2021, and she shows a video clip of the General Manager of the BIS (Central Bank of central banks), who states that, and I quote, "with the CBDC (Central Bank Digital Currency), the Central Bank will have absolute control on the rules and regulations that will determine the use of that [CBDC] ... and also we will have the technology to enforce that."

Catherine Austin Fitts then gives examples of how the CBDC's "absolute control" and the enforcement technology will inevitably manifest itself in our daily lives, and how the Covid-19 plandemic was used to soften up the masses to accept even more social control than what the bamboozled masses accepted when they fell for the Covid propaganda and scrambled to get their Covid jabs and Vaxx "passes" like good little panicked sheeple.

https://www.bitchute.com/video/RMBD3oS40S23/